Director Penalty Notices (DPNs) in 2026: What Directors and Advisors Need to Know

For directors, tax liabilities often build gradually. However, a Director Penalty Notice (DPN) immediately shifts liability from the company to the individual.

For accountants and corporate lawyers, DPNs are one of the clearest indicators that a matter has moved beyond routine advisory and into insolvency territory requiring timely intervention.

What is a Director Penalty Notice (DPN)?

A DPN is a statutory mechanism allowing the ATO to recover unpaid company liabilities directly from directors. It applies primarily to:

- PAYG withholding

- Superannuation Guarantee Charge (SGC)

- GST

The regime effectively “pierces the corporate veil,” holding directors personally accountable for amounts collected or withheld on behalf of employees and the tax system.

The Two-Phase Operation

Underlying Non-Compliance: Failure to lodge BAS/SGC statements or accumulating arrears. At this stage, risk is building but remains “contained” within the company.

Escalation to DPN: The inflection point where the director becomes personally exposed. The process is procedural and time-sensitive, not discretionary.

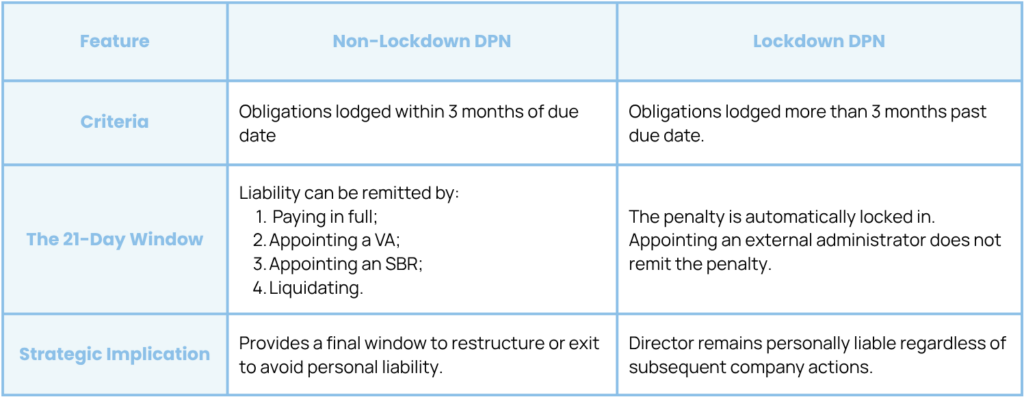

Non-Lockdown vs. Lockdown DPNs

The distinction rests entirely on lodgement timing.

The Golden Rule: “Lodge first; deal with the balance later.” Timely lodgement preserves restructuring optionality, even if the company cannot pay.

2024–2026 Trends & Practical Shifts

While legislation remains static, the ATO’s enforcement posture has sharpened:

- Faster Escalation: Shorter intervals between arrears and DPN issuance; decreased tolerance for perpetual payment arrangements.

- SGC Priority: Increased data matching has made unpaid superannuation a primary trigger for enforcement.

- Estimates & Default Assessments: The ATO increasingly issues assessments based on available data to accelerate the DPN process.

Common Misconceptions

“I resigned as a director, so I’m no longer exposed.”

Resigning does not discharge liability for non-compliance that occurred during the director’s tenure.

“If we appoint an Administrator, the problem is solved.”

Appointing an administrator only solves the DPN problem if it is a non-lockdown notice and the appointment occurs within 21 days.

“The ATO will work with us if we communicate.”

Communication does not override the law. Once a penalty is locked, the ATO has limited legislative power to waive it.

Practical Guidance for Accountants and Lawyers

Early Warning Signs:

- Deferred SGC or BAS lodgements.

- Repeated refinancing of tax debt.

- Increased ATO enforcement tone (Garnishees/Statutory Demands).

Referral Triggers:

Refer to an insolvency specialist immediately if lodgements are >3 months overdue, a DPN has been issued, or the director is unclear on their personal exposure.

In DPN matters, the difference between a successful restructure and unavoidable personal bankruptcy is often measured in days.

Final thoughts

Director Penalty Notices are not just a tax issue—they represent a shift in risk from the company to the individual.

For advisors, they are one of the clearest signals that early, specialist input can materially change the outcome.

Get in touch

If you are advising a client with unpaid super, overdue lodgements or increasing ATO pressure, it is worth having a conversation early.

We are always available to discuss situations confidentially and help map out the available options.

About the author

Greg Quin is the Managing Partner at Equinox Restructuring & Insolvency (formerly HLB Mann Judd Insolvency WA) and has been with the firm for 15 years. Greg oversees the day‑to‑day operations of the practice and the insolvency appointments managed by the Equinox team.

If you have any queries about insolvency matters, please feel free to contact Greg on 08 9215 7900, 0402 943 091 or via email to greg@equinoxri.com.au.